Frugality is the reason I got to leave.

Years of saving more than we spent, of not upgrading things that worked, of letting the accounts compound in silence — that discipline is what made it possible to walk away from a 17-year career in 2022 and move our family to Portugal. I will never talk down frugality as a tool. It built the door I walked through.

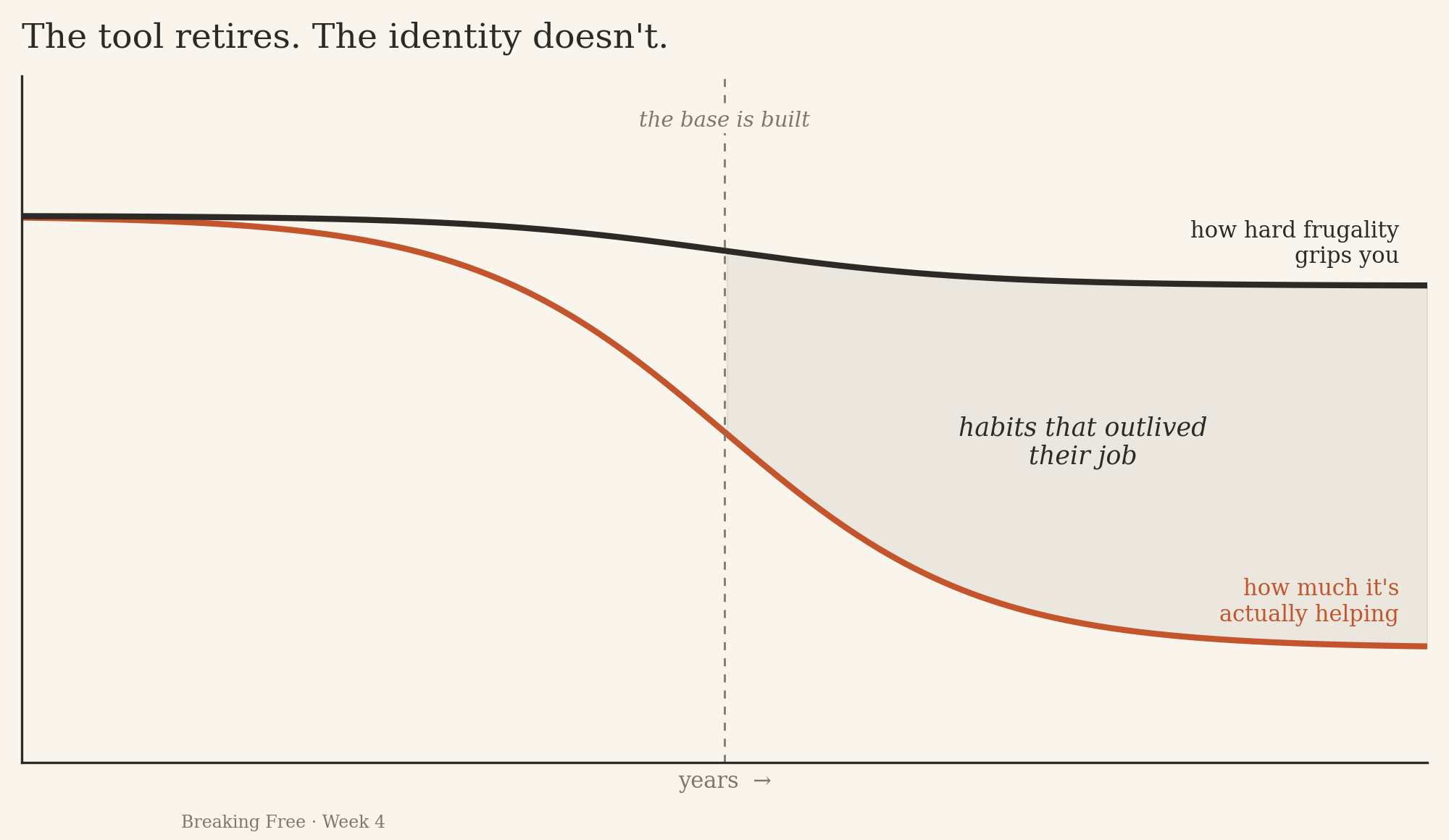

So it surprised me how long the habits outlived their job.

We moved somewhere our monthly spending dropped by more than half. The plan had worked. And I still catch myself cooking dinner at home, night after night, in a country where eating out is so affordable it barely registers — skipping the grilled fish, the new flavors, the entire point of living somewhere with food worth crossing an ocean for, because restaurants still file themselves under “splurge” in my head. Catch myself — present tense, notice. Nobody is grading me. The spreadsheet doesn’t need the win. I’m running a program written for a life I no longer live, and I haven’t fully uninstalled it yet.

That’s the trap, and almost everyone who saves seriously walks into it.

The cage you’re proud of

Tools have a quiet failure mode: use one long enough and it stops being something you do and becomes something you are.

I’ve watched smart, financially secure people live like they’re still in year two of accumulation a decade after the accumulation ended. They negotiate every bill, including the ones that cost more to dispute than to pay. They burn a weekend on a repair a professional would knock out in an afternoon — and tell you about it on Monday like they got away with something. They feel a flicker of guilt buying experiences they could fund forty times over. None of it is wrong, exactly — every habit is defensible on paper. The question that never gets asked is underneath: not why these habits made sense once, but why they’re still here.

The honest answer is usually that frugality stopped being a tool and became an identity. And identities don’t respond to arithmetic. Questioning a habit costs nothing; questioning an identity feels like threatening the self. That’s why your squirm pile from Tuesday squirmed.

The tool retires. The identity doesn’t — unless you make it.

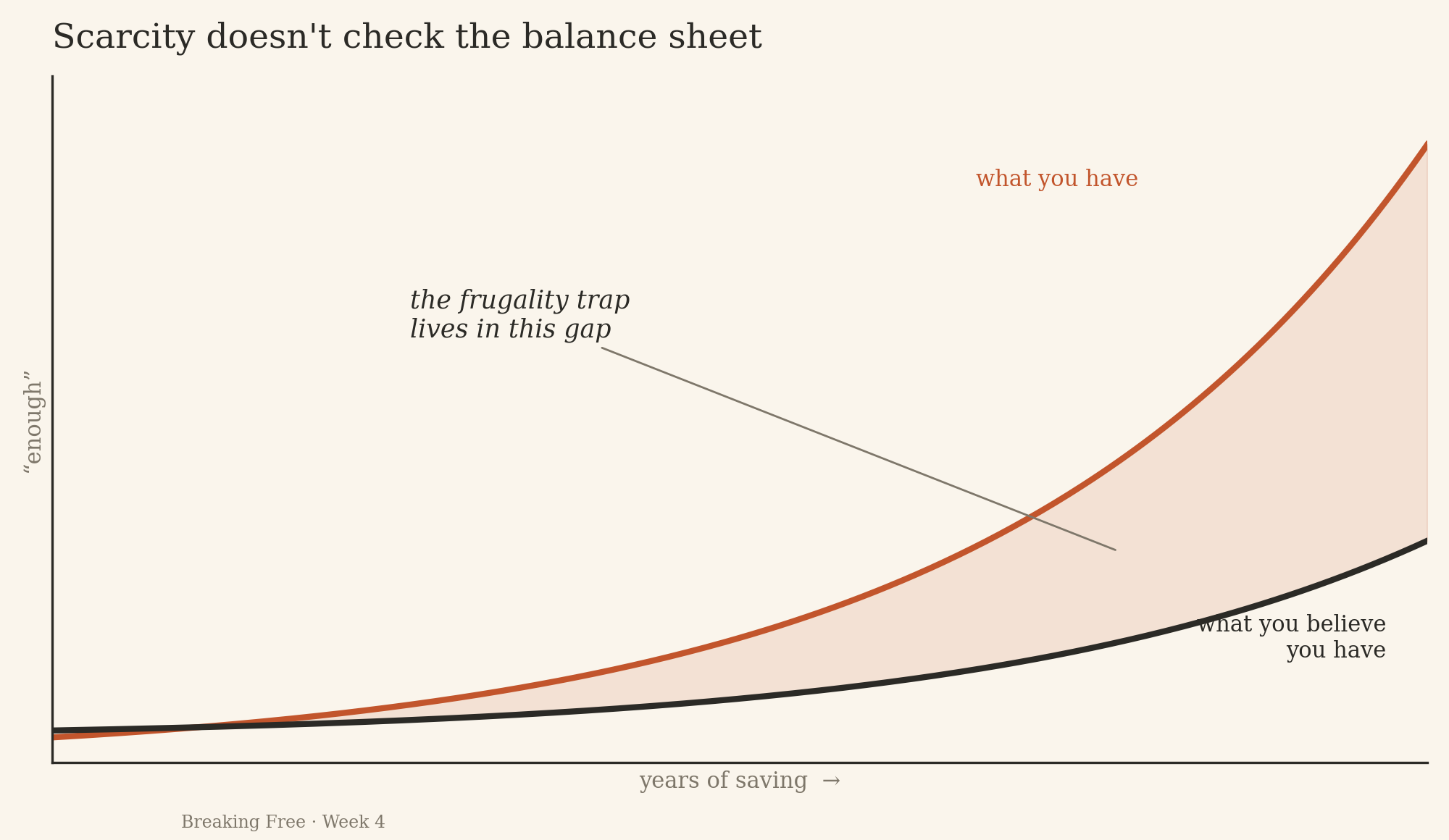

Scarcity doesn’t check the balance sheet

Here is the part most financial content skips, because it doesn’t fit in a spreadsheet.

The lived experience of not having enough — months or years of it — writes patterns that persist long after the circumstances change. You can have the portfolio, the paid-off house, the full emergency fund, and still feel the low-grade hum of what if it runs out every time you reach for your wallet. The scarcity left. The nervous system didn’t get the memo.

The trap isn’t the number. It’s the gap.

Financial freedom isn’t reaching the number. It’s the day you actually believe it. And that day doesn’t arrive automatically with the balance. It’s separate work — slower, less measurable, and nobody hands you a statement for it.

What does the gap cost while you wait? Hours spent on tasks worth a fraction of your time, to save money you could trivially afford. Trips not taken while the kids are still young enough to want to come. A scarcity you model for the people watching you — including the small ones — as if it were the permanent condition and not a phase you’re long past. The nest egg was supposed to be the vehicle. When protecting the vehicle becomes the point, you’ve lost the plot.

Try this before Sunday

Philosophy without an assignment is just mood, so here’s the assignment.

Pick one thing you’ve been deferring that you can plainly afford — the dinner, the flight, the help, the better mattress. Something real, not symbolic. Buy it this week.

I’m doing the assignment with you. Mine is a pair of genuinely good headphones — researched thoroughly, admired at length, purchased never. I’m naming it here before I’ve bought them, and I’ll report back next Tuesday. Writing it down in a newsletter is, I’m discovering, a very effective commitment device. Then pay attention to two moments: the resistance right before, and what actually happens after. The resistance is the identity defending itself. What happens after — usually nothing, no disaster, sometimes something like relief — is the evidence your number has been trying to show you.

One purchase won’t rewire you. But it starts a different kind of compounding: each act of believing the number makes the next one cheaper.

The harder question

Breaking free is not just leaving the job or the city or the structure that stopped fitting. Those are the visible exits, and they’re the easy ones to point at. The quieter exit — the one that takes longest — is leaving the story about who you have to be to stay safe.

Frugality, gripped too long, is often that story. Mine was.

The question isn’t whether you’ve saved enough. It’s whether you’ve given yourself permission to use the life you built, while you’re still in the years you built it for.

I’m not asking this at you. I’m asking it of myself, most weeks, and not always winning.

Next Tuesday I’ll tell you whether I actually did the assignment — and we’ll get into the part of buying back your time nobody budgets for. If a friend forwarded this, this is what Breaking Free does: Tuesday gives you the mechanics, Friday asks what they’re for. Subscribe and read them as a pair.

Reply and tell me: What did you buy — and what was the voice in your head saying right before you did?

— Ashleigh