First, the receipt. On Friday I told you I was finally buying the headphones. I did. Assignment complete. Your turn is coming.

Now, the post I promised back when this publication had a content calendar it was actually following.

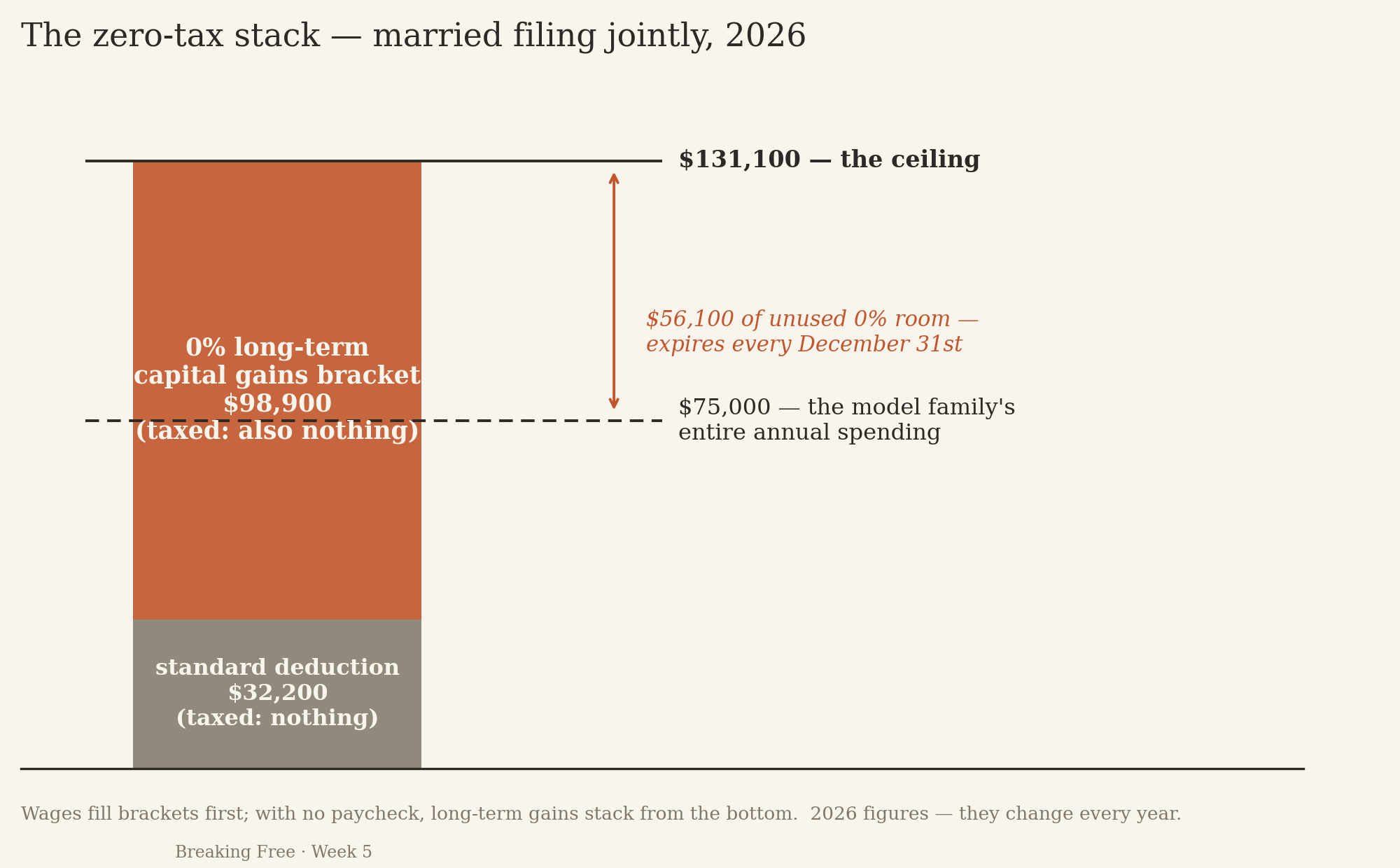

Here is a sentence that sounds illegal and isn’t: a married couple with no paycheck can realize over $130,000 of investment gains this year and owe the IRS nothing.

Not through offshore anything. Not through an LLC in a state you couldn’t find on a map. Through the plain, published tax brackets, used by people the tax code quietly favors — people who’ve stopped selling their time.

The code is written for wages

I spent 17 years collecting a paycheck, and every year the deal was the same: ordinary income, ordinary rates, withheld before I ever touched it. That’s the deal almost everyone has, and it’s why almost everyone believes taxes are a fixed cost of being alive, like weather.

They’re not. They’re a cost of earning — specifically, of trading your time for money. The year after I left, our earned income fell off a cliff, and I got to see the other side of the system up close.

The system, it turns out, has a different deal waiting for money that shows up as long-term capital gains instead of wages. You just can’t see that deal while a salary is filling up your brackets.

The stack — this is the whole trick

Capital gains don’t get taxed in isolation. They stack on top of your ordinary income, and the rate depends on where the stack lands.

So for a married couple filing jointly in 2026:

The standard deduction wipes out the first $32,200 of income. Zero tax, no receipts, nothing to itemize.

Above that, long-term capital gains are taxed at 0% until your taxable income crosses $98,900.

Add those together and the arithmetic does something most people refuse to believe on first read: roughly $131,100 of realized long-term gains, completely federal-tax-free — if no wages are filling the brackets first.

(Those two numbers change every year with inflation. The logic doesn’t. Verify the current figures before you act — they take thirty seconds to look up.)

The 2026 stack for a married couple: $75K of spending doesn’t even reach the ceiling.

The $500K / $75K model

Now make it concrete. Say you’ve built a $500,000 taxable account on top of your retirement accounts, and your family spends $75,000 a year.

You stop working. You sell $75,000 of long-held index funds to live on. Part of that sale is your own money coming back to you — basis, never taxable. Only the gain stacks into the brackets, and it lands far below the $98,900 line.

Federal tax owed: zero. Not “low.” Zero.

And here’s the move that separates the playbook from mere luck: in those low-income years, you can choose to realize more gains than you spend — sell, pay 0%, immediately rebuy, and reset your cost basis higher. The gap between your spending and the 0% ceiling is free tax-erasure, and it expires every December 31st. Most people in low-income years — a sabbatical, a layoff, a transition, an early retirement — let it expire unused, because nobody told them it was there.

The Roth ladder, in one paragraph

Same low-bracket years, second lever. Money trapped in a traditional 401(k) or IRA can be converted to Roth a slice at a time. Convert just enough to fill the standard deduction and the bottom brackets, pay little or nothing on the conversion, wait five years, and that money comes out tax-free forever — decades before age 591/2. That’s the bridge most early retirees use, and it only works because their taxable income is low enough to make conversions nearly free. The window is the asset.

Before you fire your accountant

Three honest caveats, because this is a playbook, not a brochure. State taxes don’t all follow the federal script — Portugal and California have opinions, and so does wherever you live. If you buy health insurance through the ACA marketplace, realized gains count as income and can shave your subsidy, which is a real cost wearing a disguise. And every figure above is a 2026 number that will be different next year.

The usual reminder, plainly: I’m not your tax advisor and this isn’t personalized advice — it’s the durable logic, which is the part worth learning.

This week: find your gap

The takeaway isn’t “quit your job for tax reasons.” It’s that low-income years are assets, and most people waste them. So, twenty minutes:

- Pull your last tax return and find your taxable income (after deductions).

- Subtract it from the current 0% capital-gains ceiling for your filing status. That number is your gap.

- If you’re in — or heading into — a low-income year and you hold appreciated investments in a taxable account, that gap is what you could harvest at 0%. Write the number down. Ask your tax person one question: “what would it cost me to use this?”

Most people pay for tax advice on how to earn more efficiently. Almost nobody asks what their non-earning years are worth.

The tax code doesn't reward the rich as reliably as it rewards the patient.

Friday: the harder half of FIRE — what happens when you win the freedom and have no idea what it’s for. The money math is the easy part. See you then.

Reply and tell me: Have you ever had a low-income year — sabbatical, layoff, transition — and did anyone tell you what it was worth?

— Ashleigh