There’s a moment most people in finance never name clearly, even though everything downstream depends on understanding it.

It’s the moment your invested capital — quietly, without asking your permission — starts growing faster than your take-home pay.

Not larger than your salary. Larger than the growth of your salary.

If your portfolio earns 8% on $250,000, it grew by $20,000 last year. If your raise was $4,000, you added more wealth by sitting still than by getting promoted. The machine is now doing more work than you are.

That’s the tipping point. And once you cross it, the job is never quite the same thing again.

What changes at the crossing

Before the tipping point, your paycheck is your primary wealth-building engine. Every financial decision gets filtered through it: does this help me save more, invest more, earn more? The job isn’t just income — it’s the load-bearing wall.

After the crossing, the job becomes one of several engines, and not necessarily the most powerful one. Your capital is now working a full shift beside you. This changes the negotiation — with your employer, but mostly with yourself.

You stop needing a raise for survival. You start asking whether the raise is worth what it costs. Longer hours, a bad manager, a role that doesn’t fit anymore — the price goes up because the need went down.

That’s not a reason to quit. It’s a reason to choose.

The people who cross the tipping point and don’t notice it keep playing the before-the-crossing game indefinitely. They negotiate for raises they don’t need, endure conditions they don’t have to, and never realize the game changed.

The math, made concrete

The better your investing chops, the lower your tipping point. With just $1M in a taxable brokerage, a 13% return can generate $130K a year — and if you read last week’s article, you’d know exactly how you can pay 0% federal tax on that income.

For the reader who doesn’t have their number handy, here’s the framework:

Take your current investable net worth — taxable accounts, retirement accounts (the order you fund those still matters), anything earning a return. Multiply by your honest expected long-term return (I use 7% real, because I’m not in the business of promising). That’s your portfolio’s annual “paycheck.”

Now compare it to the amount you actually add to savings from your job — not your gross salary, your net savings rate.

If your portfolio paycheck is close to or larger than your savings contribution, you’ve crossed. Or you’re close.

Most people who’ve been saving seriously for 15-20 years are closer than they think. They just never ran the number.

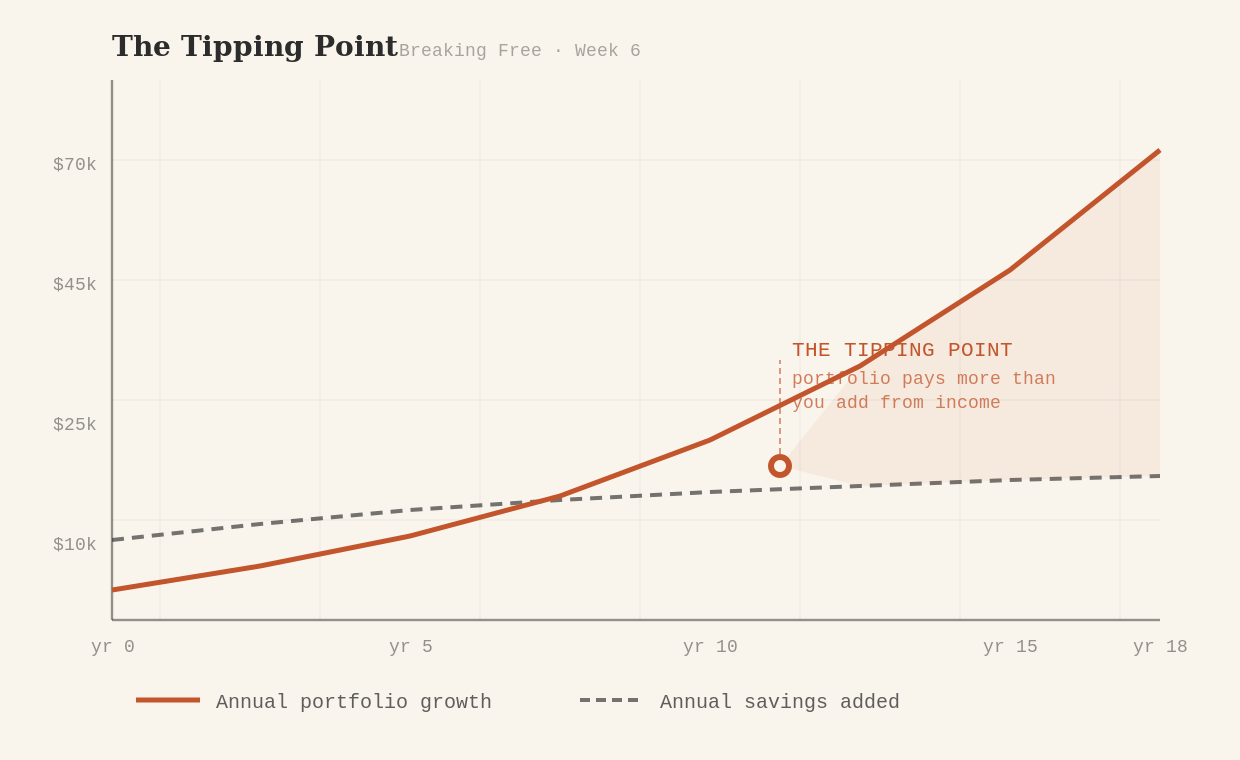

Two lines crossing: annual portfolio growth (rising) vs. annual savings contribution (flatter). The crossing is the tipping point — somewhere between years 12 and 20 for a consistent saver.

Two lines crossing: annual portfolio growth (rising) vs. annual savings contribution (flatter). The crossing is the tipping point — somewhere between years 12 and 20 for a consistent saver.

The hour revaluation

Here’s the thing that doesn’t get said enough after the crossing: your time’s highest and best use shifts.

Back in Week 1, we talked about the exchange rate between money and time — and how most people never check it. The crossing is where that rate changes most dramatically.

Before the tipping point, an hour of overtime probably generates more wealth than an hour spent studying your portfolio. The paycheck is the lever.

After it, that calculation quietly inverts. An hour spent understanding your tax situation — running a Roth conversion, harvesting a loss, calculating the gap to the 0% bracket — can be worth more to your net worth than a full day at the office. And buying back your time from low-value tasks isn’t just about hiring a cleaner anymore. It’s about reclaiming the hours that could be compounding instead of clocking in.

This isn’t an argument to stop working. It’s an argument to stop assuming the office deserves all your best hours just because it always did. The portfolio is now a business that requires management — and it pays you for the attention.

The subtler version of the tipping point

There’s a version of this that isn’t about the math.

It’s the moment you believe the math.

I knew the numbers probably worked before I left my career. I’d run spreadsheets. I’d read enough. But the knowing and the believing are different, and I’m not sure you can reason your way to the believing. You kind of have to sit in it, test it, watch the account statements for a year or two, and let the reality catch up to the model.

The gap between knowing and believing is where most people stay stuck. They have enough. They can’t feel enough. So they keep adding another year, then another — which is just a different version of the question we asked in Week 3: optimizing for what, exactly? And it’s the same psychology as the frugality trap: the habits that built the machine keep running it long after the machine has done its job.

Your number this week

Two steps, twenty minutes:

- Calculate your portfolio’s annual “paycheck” — current investable assets x your expected real return. Write it down.

- Calculate your annual savings contribution — what you actually add to investments each year from income. Write that down too.

If step 1 is already larger: you’ve crossed. The job is mathematically optional. What you do with that information is a different question, but you deserve to know it.

If step 1 is smaller: you know exactly what you’re building toward and roughly how far you are from the line.

Either way, you stop guessing and start knowing. And knowing changes something.

Friday: the social arithmetic of breaking free — because you can win the financial game completely and still find yourself broke in the ways that matter. Community is the asset most freedom-seekers forget to build.

Reply and tell me: When did you run this math for the first time — and what did you feel when you saw the number?

— Ashleigh